The economic x-ray of the Milei era

The Argentine economy has for decades been a laboratory for studying the effects of chronic inflation and stagnation. For any analyst, the success of a stabilization program is not measured only in the offices of international organizations, but must be reflected, fundamentally, in the purchasing power of ordinary citizens. Today, recent data allows us to put together both pieces of the puzzle: macroeconomics and microeconomics.

Macro support: World Bank projections

To understand the change in expectations, just look at the recent international forecasts. According to the latest economic update report for Latin America and the Caribbean from the World Bank, the organization has highlighted the performance of the Argentine economy with extremely optimistic projections: it anticipates a growth of 3.6% for this year (2026) and 3.7% for 2027.

This data becomes more relevant when compared to its regional environment. While Argentina projects this rebound, the average expected growth for the region stands at a modest 2.1%. Even more revealing is the organization’s calculation on the medium term: the estimated accumulated growth for the entire mandate of Javier Milei’s government would reach a resounding 12.2%. To delve deeper into the sectoral composition and the technical bases of this recovery, it is essential to analyze the official report on the evolution of GDP prepared by INDEC.

However, macroeconomic growth would be just an abstract number if it did not translate into social well-being. This is where the second key indicator comes into play: salary.

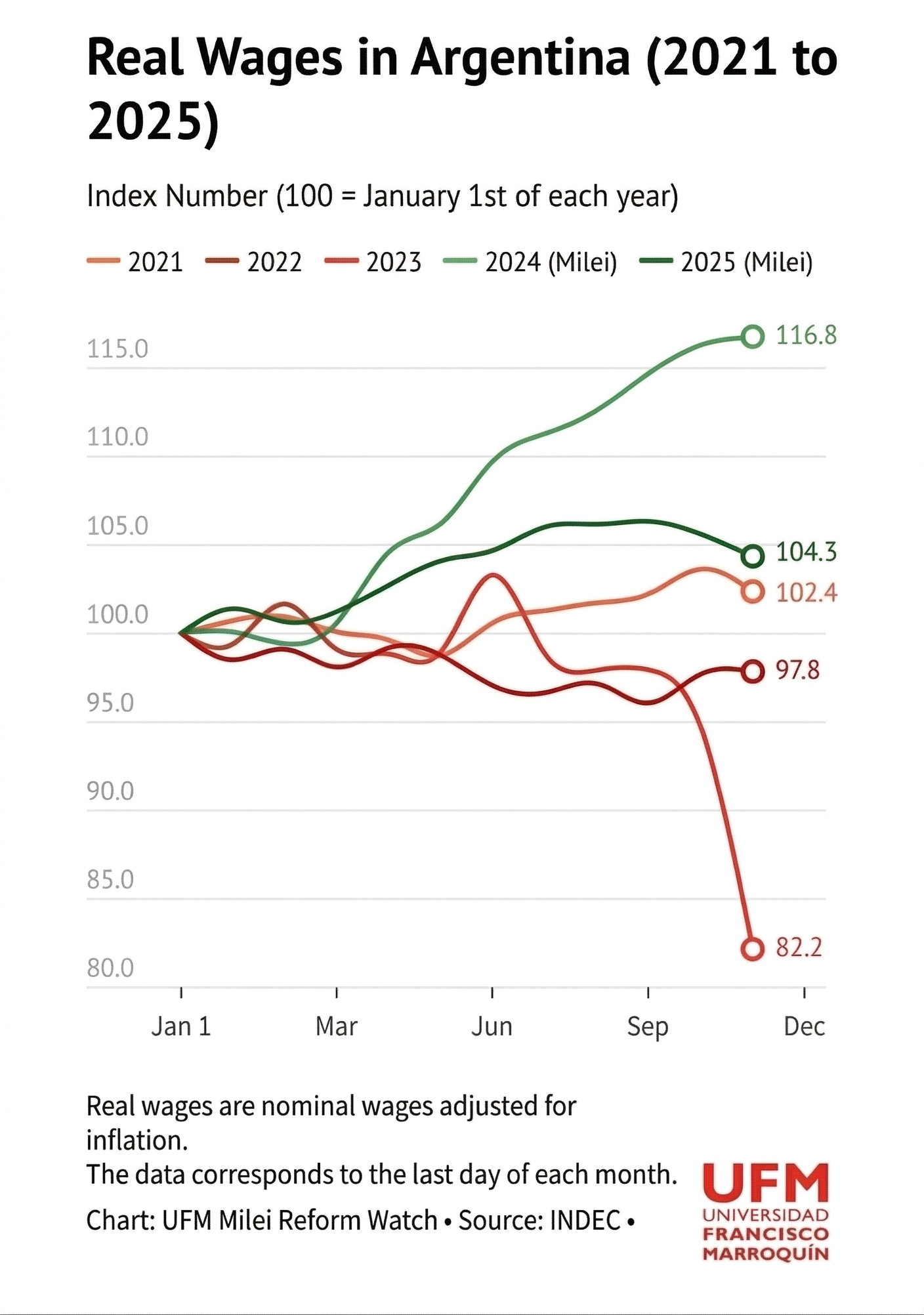

The micro impact: The recovery of real wages (2021-2025)

Recently, the UFM Milei Reform Watch observatory, using official databases, published a graph that illustrates the trajectory of real wages in Argentina from 2021 to 2025. The analysis of these curves offers us a clear image of how the initial shock impacted—and then benefited—pockets.

The chart uses a base index where January 1 of each year equals 100, allowing us to see salary performance within each calendar year.

- The erosion of the previous model (2021-2023): In 2021 and 2022, real wages showed stagnation (closing at 102.4 and 97.8). But the collapse is evident in the 2023 red line, which shows a dramatic drop to an index of 82.2 in December, reflecting the disclosure of repressed inflation during the change of administration.

- 2024, the year of the turn: Despite the harsh initial adjustment where the real salary remained below the 100 index until March, the trend was reversed. The year closed at 104.3, showing that salary updates began to win the race over prices in the second half of the year.

- 2025, the takeoff of purchasing power: The dark green line shows uninterrupted growth since January, reaching an index of 116.8. This 16.8% increase in real wages within the same year suggests that disinflation generated a genuine increase in workers’ wealth.

Conclusion: From stabilization to growth

In economics, the trend often matters as much as the absolute value. What international reports and microeconomic analysis demonstrate is a consolidated regime change.

It has gone from a scenario of chronic deterioration to a phase of dual expansion: the macroeconomy projects to lead growth in the region, while the reduction in inflation is rapidly returning purchasing power to wages. While structural challenges remain, the alignment of these two factors suggests that the stabilization program is beginning to deliver its most tangible fruits.

Calculate your FIRE number

Find out if your portfolio would survive the worst crises in history with our free Monte Carlo calculator.

Try the simulator