What is the FIRE Movement? The Guide to your Financial Independence

- What exactly does the acronym FIRE mean?

- The math behind FIRE: The 4% Rule

- How to calculate your “FIRE Number”?

- The 3 Pillars of the FIRE Movement

- 1. Extreme Savings and Expense Optimization

- 2. Aggressive Income Increase

- 3. Smart Investment

- Different “Flavors” of the FIRE Movement

- The Enemies of Early Retirement

- Is the FIRE Movement for you?

Have you ever wondered what your life would be like if working were an option and not an obligation? For decades, the traditional script dictated that we should study, work hard for 40 years, save a little, and wait until age 65 to finally enjoy our time.

However, a growing global community has decided to completely rewrite these rules. We are talking about the FIRE movement, a phenomenon that has gone from being a niche in internet forums to a true revolution in personal financial planning.

If you are looking to take control of your financial future, understanding what FIRE is and how its underlying mathematics works is the essential first step.

What exactly does the acronym FIRE mean?

FIRE is an acronym that stands for Financial Independence, Retire Early. Although they are often pronounced together, they represent two very different concepts:

- Financial Independence: It is the exact point at which the passive income generated by your investments is enough to cover all your living expenses. At this point, you are no longer dependent on a monthly salary to survive.

- Retire Early: It is the conscious decision to leave traditional employment before the legal retirement age (often at age 30, 40 or 50).

It is vital to understand that within the community, the main focus is always on the first part (FI). Achieving the freedom to decide what to do with your time is mandatory; stop working completely (RE), is totally optional.

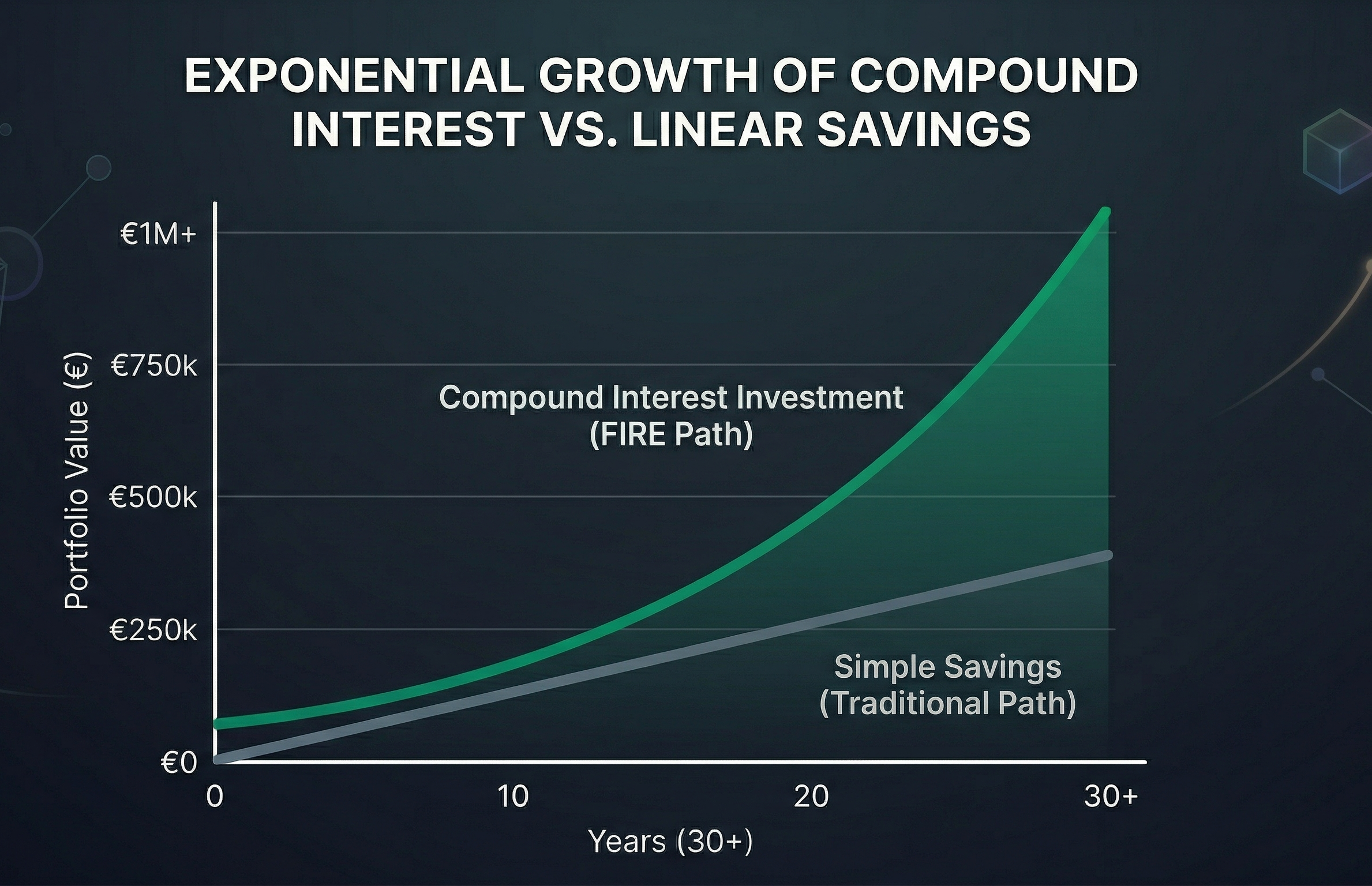

The math behind FIRE: The 4% Rule

The FIRE movement is not about winning the lottery or magical get-rich schemes. It is based on pure financial mathematics, compound interest and long-term planning.

The central concept that supports the viability of early retirement is the famous 4% Rule, originating from the historic Trinity Study. This study analyzed the behavior of the stock and bond markets over decades to answer a key question: How much money can I withdraw from my portfolio each year without risk of running out to zero?

The conclusion was that, historically, if you withdraw 4% of the initial value of your portfolio during your first year of retirement and adjust that amount annually for inflation, your money should last at least 30 years, even in periods of serious economic crises.

How to calculate your “FIRE Number”?

Calculating how much money you need to be financially independent is surprisingly simple at its initial stage. You just need to apply the inverse of the 4% Rule, multiplying your annual expenses by 25.

Formula: Annual Expenses x 25 = Your FIRE Number

For example, if your living expenses are €30,000 per year, your FIRE number would be €750,000 (30,000 x 25 = 750,000). Once your investment portfolio reaches that number, you will have crossed the finish line.

The 3 Pillars of the FIRE Movement

To reach that “FIRE Number” in record time, practitioners of this movement rely on three unbreakable pillars:

1. Extreme Savings and Expense Optimization

While traditional financial advice suggests saving 10% or 20% of your income, the FIRE community targets savings rates of 40%, 50%, or even 70%. This does not mean living in misery, but rather practicing “conscious frugalism”: ruthlessly eliminating expenses that do not bring real happiness and optimizing key items such as housing, transportation and food.

2. Aggressive Income Increase

You can only cut expenses to a certain point. To accelerate the process, it is essential to maximize capital inflow. This is achieved by negotiating promotions, moving to better paying sectors or creating additional sources of income (side hustles).

3. Smart Investment

Saving money in the bank is a sure recipe for losing purchasing power due to inflation. Money must be put to work through compound interest. The preferred vehicle for the FIRE movement is low-cost index funds that track global indices (such as the MSCI World or the S&P 500), diversifying risk and capturing long-term global economic growth.

Different “Flavors” of the FIRE Movement

Over time, the movement has evolved to accommodate different lifestyles, as not everyone aspires to the same level of spending or desires the same type of retirement. Today there are several “flavors” of FIRE:

- Lean FIRE: For those who plan to live on a very tight budget (generally less than €25,000 annually). It requires a much smaller portfolio and allows for very quick withdrawal, but demands a highly frugal lifestyle.

- Fat FIRE: Quite the opposite. Designed for those who want a retirement full of luxuries, travel and comforts (expenses greater than €100,000 annually). It requires massive capital and therefore very high wages during the accumulation stage.

- Barista FIRE: This involves saving enough so that your investments cover much of your expenses, but you decide to keep a part-time (or low-pressure) job to cover the rest and often get health insurance.

- Coast FIRE: You reach an invested amount at an early age that, thanks to compound interest, will grow on its own to form your FIRE number by traditional retirement age. From that moment on, you only need to work just enough to cover your current expenses, without needing to save another cent.

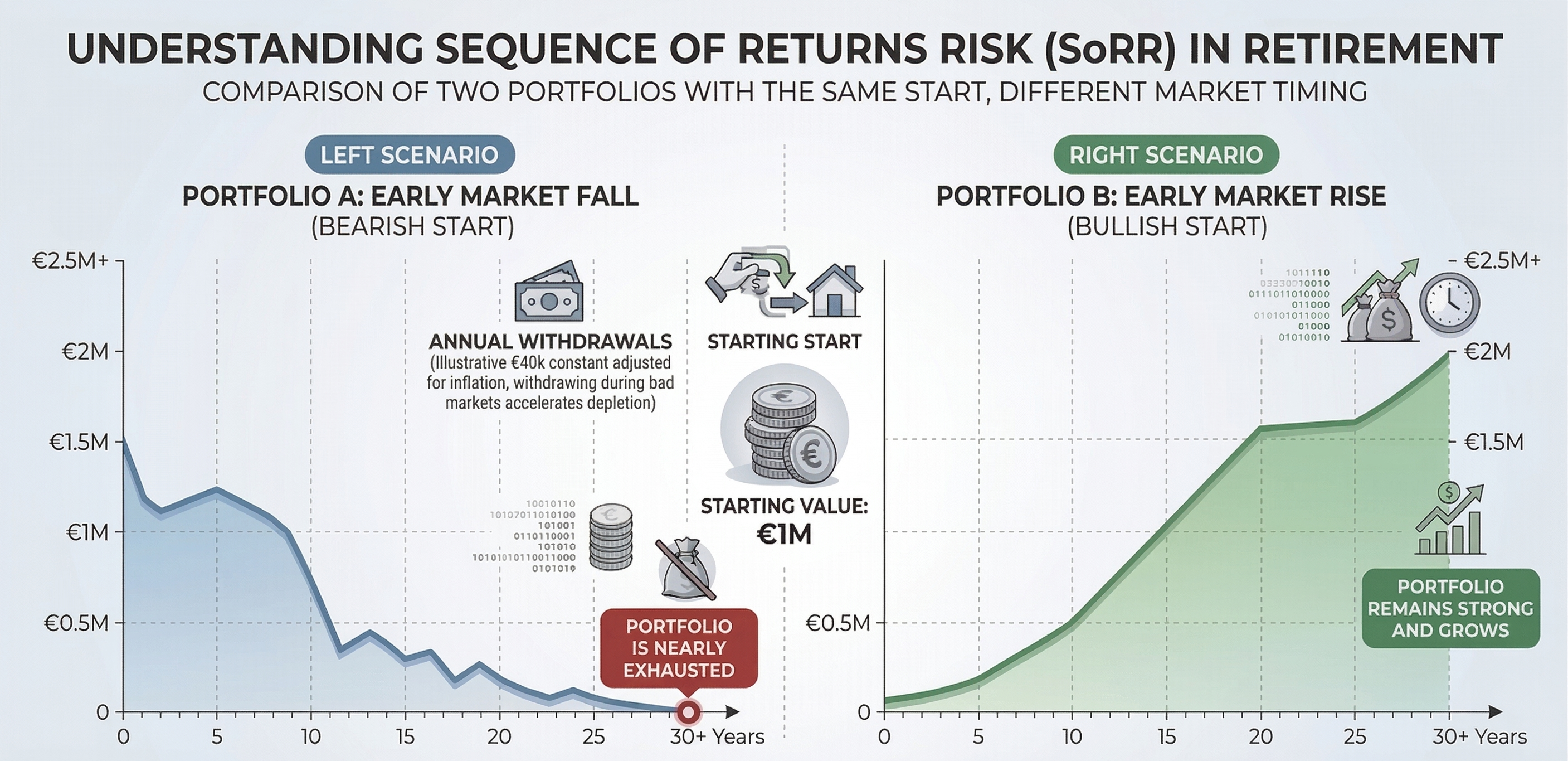

The Enemies of Early Retirement

Planning for a 40- or 50-year retirement is not the same as planning for a 20-year one. Although the 4% Rule is an excellent starting compass, financial mathematics forces us to be much more rigorous when we leave our jobs young. You have two great enemies:

The first is inflation, that silent devourer that erodes the purchasing power of your money. Your plan should assume that life will be noticeably more expensive two decades from now.

The second, and more dangerous, is Sequence of Returns Risk. If the financial markets take a big downturn during the first few years of your retirement, you will be forced to sell your investments at low prices to pay your bills. This can deplete your portfolio prematurely, a mathematical damage that is almost impossible to recover from.

This is why simple spreadsheets are not enough when your retirement date approaches. You need to stress your plan. To do this, we highly recommend using our free Monte Carlo simulator. This advanced tool will subject your portfolio to thousands of economic scenarios and historical crises to check if your withdrawal strategy is truly resistant to the passage of time and the worst market storms.

Is the FIRE Movement for you?

The FIRE movement is not an easy path. It requires discipline, initial sacrifice, a high tolerance for social nonconformity and a solid education in personal finances.

However, its mathematical principles are universal. Even if you don’t have the desire to retire at age 40, applying the philosophy of optimizing expenses and constant investment will provide you with an immense security cushion. At the end of the day, the FIRE movement is not just about money; It’s about buying back the most valuable and irrecoverable asset you have: your time.

Calculate your FIRE number

Find out if your portfolio would survive the worst crises in history with our free Monte Carlo calculator.

Try the simulator